Reinsurance Law & Practice

The Insurance Industry operates on the principle of sharing of risks. Insurers cannot operate if their risks are not shared amongst Co-Insurers and Re-Insurers.

This is because the availability of reinsurance enables an insurer to accept risks that would otherwise be beyond its underwriting capacity by allowing the ceding insurer to “reinsure” a portion of the risk/loss, and at the same time spread the risk of a major loss. Reinsurance, in simpler terms, is the insurance of an insurer by another insurer.

Some large organizations organize their insurance and risk programmes within their organisations through captive insurance. Shell is one such organization. A captive is essentially a wholly-owned insurance company, usually located in a jurisdiction where taxation, solvency and reporting requirements are relaxed. They are usually managed by specialist companies that act as accountants and administrators.

The principles of insurance apply similarly to a reinsurance transaction, among others being the contract of indemnity creates an insurable interest in the property and that parties are responsible to ensure the duty of utmost good faith is upheld

“A reinsurance contract is one where an insurance company passes a proportion of its obligation under the main insurance contract to another insurance company”

In a general insurance arrangement, an insurer would typically indemnify its original insured under a specific insurance policy. Reinsurance comes into play when the insurer becomes the reinsured, seeking to insure the risk of its original insured to another insurer (the reinsurer) in order to spread the risk which it had agreed to indemnify. The risk may then be passed/ ceded to another insurer, commonly referred to as retrocessionaires.

Reinsurance is also available for Islamic or Takaful Insurance. Reinsurance of Takaful is called ReTafakul, the contents and coverage will in many cases be similar.

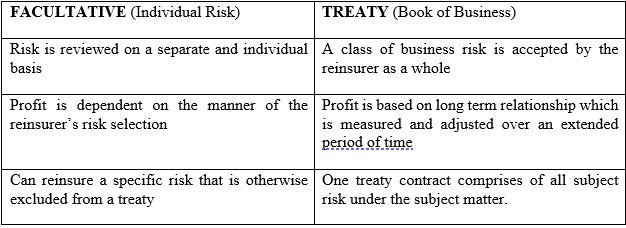

The manner in which reinsurance is accepted by a reinsurer can also be categorized into 2 main forms being facultative reinsurance and treaty reinsurance. The manner in which reinsurance is underwritten would normally depend on the market’s demand. Treaty reinsurance can be equated to a reinsurer accepting the entire risk of a particular class. An illustration would be if A were to reinsure B, in particular for any loss arising from the headlights of C-type cars for the year 2018.

In this example, the tires or the engine of the C-type cars may be reinsured with a different reinsurer, D, for the year 2018.

As for facultative reinsurance, it is designed to protect a specific risk underwritten by the reinsured. Facultative reinsurance would be an easier concept to grasp whereby the reinsurer would agree to indemnify a specific risk of a particular insured for a certain expressed period. In other words, facultative reinsurance agreements/ contracts cover individual underlying policies and are written on a policy/ risk specific basis, Because this type of reinsurance is usually applied for unusual risk exposures, the terms and conditions are individually negotiated between parties, separate from the terms of some other reinsurance contract. For example, when B agrees to indemnify C’s oil rig construction project, A may reinsurer B, in particular, for losses to be suffered by C arising from bad weather or rough sea conditions.

In all instances, the payment of premium would form a substantial part of the contract, being the consideration to be paid by the reinsured for risk accepted by the reinsurer, without which the reinsurance coverage would not be operative. Under a reinsurance contract, the reinsured, also the insurer, would pay a particular sum as premium to its reinsurer in return for future reimbursement of the reinsurer’s portion of the risk exposure of the original insurance policyholder. Premium payments would also relate to parties responsibility towards the duty of utmost good faith, which is a trite principle in insurance and reinsurance.

Would you like to read more?

The Impact Lawyers offers a FREE newsletter that keeps you up to date on news and analysis about the international latest legal news.

Please complete the form below and click on subscribe to receive The Impact Lawyers Newsletter subscription

Related links

Main menu